April 19th, 2017 by MSI Newsletters

Rate Structures

Filed in: Monthly Newsletters |

Previously we went into a very detailed, multi-page, explanation of some different structures and we wanted to give a summarized refresher. In this article, we will focus a little time to flat rate merchant processing, tiered and Interchange plus with the primary pro and con for each.

Basics of industry pricing:

All credit card processors are charged a fee by the card issuers for moving money, called interchange. Interchange is currently made up of over 800 card and charge type combinations ranging from 0.05% + $0.22 up to 3.25% +$0.10 per transaction. The processing industry built different pricing structures for several reasons, most primarily to simplify the costs to the merchants. Now that you know a little about the basis of the structure let’s look at a couple different structures.

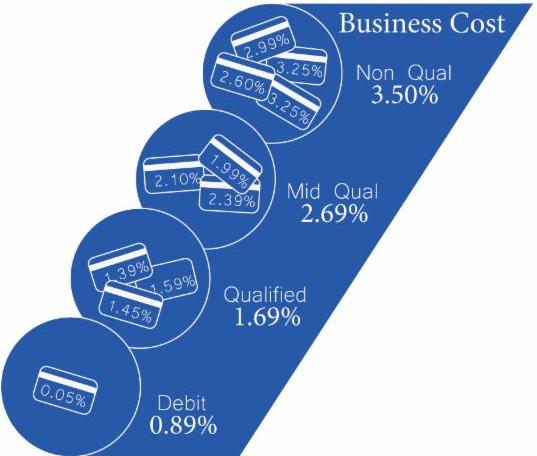

Tiered and Flat Rate Pricing Structures:

The tiered rate plan has always been a popular option, generally consisting of 4 or 5 different rates based on the transactions processed. Basically, the processor takes the 800+ possible rates and groups them together into buckets and charges the merchant one rate for each bucket. It’s much easier to explain to a merchant how a card type, or method of acceptance will be billed at one of a few rates than explaining interchange.

![]() Companies like Square use the tiered structure to charge merchants based on how they accept a card. Quick example: swiped transaction process at 2.75% and keyed transactions process at 3.50% + $0.15. While is this referred to as a flat rate setup, it’s actually a two tier account. They just use the two tiers to simplify the cost of card acceptance.

Companies like Square use the tiered structure to charge merchants based on how they accept a card. Quick example: swiped transaction process at 2.75% and keyed transactions process at 3.50% + $0.15. While is this referred to as a flat rate setup, it’s actually a two tier account. They just use the two tiers to simplify the cost of card acceptance.

Pro:

Simplified fee, which are easier to understand and easier to estimate processing costs

Con:

As the merchant you can’t tell how much you’re paying to your processor and how much is going to interchange.

This structure has been around forever, however has become more mainstream in the past 10 years. In this structure the processor doesn’t bucket anything, it simply passes the interchange cost from each transaction processed to the merchant and then separately tacks a small flat rate on top. It can be difficult to wrap your head around the idea at first, just due to the number of possible fees, however in either structure you are paying for interchange, this one just shows you what the issuer charged to move the funds.

This structure is very transparent, in that you will see exactly what you paid in interchange and what you paid to your processor. This allows you to better control your merchant processing costs, however your trading a little bit of simplicity for better control.

Pro:

Almost always more cost effective, and easier to know where who is getting your processing fees

Con: It’s a little more difficult to understand, and adds some additional complexity to processing statements

So, which is better?

It’s almost always Interchange Plus, in fact there are only two ways tiered beats it.

1.The plus side of your Interchange Plus account is inappropriately high, which can be resolved by shopping around.

2.Your processor was not effective in setting up their buckets and they basically don’t have any margin on the buckets. (Quite unlikely)

I’m not saying you can’t have a fair setup either way. I have seen plenty of tier accounts that were very cost effective, however if I were looking at change providers I would only be looking an interchange plus structure.

How do I know if my current setup is competitive?

You need to start by figuring out what your total processing volume and your total monthly fees are for a given month. If you divide your total merchant account expense by your processing volume you will end up with your effective rate.

Example: If you processed $12,152.79 last month and the total fees were $392.54 you effective rate was 3.23%.

$392.54 / $12,152.79 = 0.0323 or 3.23%

Now if you are happy enough with that percentage and don’t feel like shopping around at least you know what that month costed you. If you want to shop around you now have a basis of comparison. When you receive a quote from a processor is should include an estimate of what your dollar volume is going to cost using their service and you can calculate the effective rate of that quote to compare against your own.

Something to keep in mind: The lower your processing volume the higher your effective rate maybe due more static fees. Regularly checking your effective rate against your volume is a good idea to stay on top of your effective cost.

Send us an email with your statement and let us do the breakdown for you and give you our opinion of your current setup and how your payment types are affecting your processing fees. There are many instances where changing an internal business process will do a lot to lower your effective processing costs even before changing your rates.