At its heart PCI requirements are a set of standards designed to make sure all companies in the payment chain are handling cardholder data in a secure environment. Having a structured requirement like PCI can feel like a burden to many small businesses however it pails in comparison to the burden of operating in a world without it. PCI was once explained to me as something that can’t make a business completely secure, however, it will assist businesses to take small incremental steps in securing their businesses. Sure a business might get through the Self Assessment Questionaire the first year and still not have implemented most of the best practices, however, if they implement a few each year they are going to be big strides over time.

At the time I thought that was a fair point, however, the person telling me worked for the company getting paid to handle compliance. That said over the years we have seen our customer base become much savvier about securing their customer’s data. Sure there are still questions in the Self Assessment Questionnaire(SAQ) that seem to stump everyone, but the fact they get stumped means they are thinking about the questions. People who blindly guess at answers don’t tend to get stumped.

Over the years PCI has prevented fraud, which is something you can’t really quantify. I know for many PCI seems like a pain, but have a breach as a small business and see how your customers respond to it… See how burdensome your payment processing becomes with fines and additional requirements. Most businesses don’t realize that PCI has likely already prevented an issue in their business. Maybe you can find a merchant who claims to have never done PCI and they don’t know a thing about it, but I bet you can still find ways that PCI has helped that merchant. From changes made in computer network hardware, the merchant’s own payment device(s), how the other businesses in the area operate, and of course, changes made at the processor level.

To this day I am still not thrilled about the PCI process. The SAQs are generally to long, some questions incomprehensible, and the vulnerability scan is way outside the scope of many merchants. I wish all of those things would change for the better, however, looking back on PCI since it originally came out in late 2004 I have to say even as complicated as it is, it seems to have done a lot of good.

If you are one of the businesses that gave up on trying to complete your PCI, I recommend you give it another go. PCI support as improved industry-wide and the benefits over time greatly outway the hour or two of annoyance. I agree it’s definitely not as good as it could be for small businesses, but it still beats the alternative.

If you have a merchant account then you have likely heard the term interchange, but many don’t quite understand what it is, how it works, and why it matters. We are going to generally cover the basics of interchange so everyone has a basic understanding of what it is and how it works. First, let’s start off simple.

Simple Explanation:

Interchange defines what card issuing banks charge payment processors for moving funds. It is set across the payments industry so all payment providers have the same interchange costs. It is also the prevailing cost to payment providers when looking at transactional expenses. Rates and fees merchants pay may not explicitly state the interchange cost however it is baked into the fees charged to merchants when processing payments.

Let’s dig in some more:

Interchange is best represented as a matrix and is made up of more than 800 different card types and card type combinations. Each combination may have its own rate generally speaking between 0.05% + $0.21 to 3.25% + $0.10 per transaction.

Card types refer to not only the band the card is associated with, like Visa or MasterCard, but also include it is credit or debit, or what program the card is associated with. MasterCard World Elite and MasterCard Business World Elite are two different card types and their transactions may be processed at different interchange costs.

Charge types refer to the different factors involved when running a particular transaction. There are many factors that can come into play, the most basic being, if a transaction was keyed in or processed via EMV, or if address verification was attempted. That said it could include the type of business processing the card as well as how old the authorization was before it settled. You can imagine where this could get very complicated. For example, you could take the same card twice and the interchange cost on that transaction could be different each time just due to differences in how you had to accept that card. Or two different businesses could accept the same card the same way and end up with different interchange rates. Couple that with all of the different card types and you end up with a mess of combinations.

There are some interchange combinations that do not appear at first glance to fit into the rate range mentioned above. For example, GSA Large Ticket has an interchange rate of 1.20% + $39.00 that said it’s a very specific type of government transaction, and while a $39 transaction fee seems crazy you have to note that it only applies to sales over $5,900 which is equivalent to 0.66% on top of the 1.20%.

Costs Trickle Down:

What many merchants seem to miss is that the interchange costs trickle down. It doesn’t matter what pricing structure a merchant has, the interchange fees are covered by the merchant. Sure you may have a flat percentage fee for EMV transactions, but rest assured interchange was already calculated in. Also if a large enough group of merchants is doing things that cause the effective interchange cost to increase enough the payment provider will just adjust the pricing accordingly. At the end of the day, it’s in everyone’s best interest to process payments effectively as reasonably possible.

If you can accept payments in person EMV and NFC-based transactions are going to get you started down the most cost-effective road. Make sure you are settling your transactions at the end of each day, as authorization that has aged over 24 hours may result in a higher interchange cost.

If you are eCommerce or a business that keys all of its sales you will want to make sure you are using address verification and CVV.

In addition, make sure your processor is doing what it can to help you lower your interchange costs. Some processing systems, like our own, look at the transaction data to see if it can provide additional information at the time of settlement to shift transactions into a lower-cost interchange category. For some merchants, this can generate significant savings.

Interchange Padding

While the interchange tables are the same for all processors the cost to the merchant isn’t always the same. Some payment providers use a technique that many refer to as interchange padding. This questionable practice is used to make the fees charged by the processor appear smaller. Basically, the processor makes it look like they are passing interchange costs directly to the merchant, but in reality, they are inflating those costs on the merchant’s statement. To the merchant, it looks like they are paying true interchange when they are not. This is most commonly seen on interchange plus, or cost plus, fee structures. While it is somewhat rare to run into this these days it still happens.

In order to see if there is interchange padding on your account, you have to look up each card and charge type you were billed for and compare it against the current interchange table.

If you find discrepancies its worth a call to your processor to ask about it. It could be you are not looking at the correct card and charge type. This is common as the merchant statements generally use vague descriptions of the charge type which can make things difficult to look up. If you find the processor is padding interchange I would recommend shopping around.

Keep in mind this is generally not something your sales agent would have control of and may not even realize is going on. If you have an agent you have been working with it’s a good idea to point these practices out to them. At the end of the day, most agents don’t want to be associated with such practices, and bringing it to their attention will help them in the long run. Plus if you have a good agent you have been working with they likely will be able to assist you in shopping around.

Visa and MasterCard’s Interchange Tables

The interchange tables are published publicly for everyone to see. Here are the most recent Visa and MasterCard tables I was able to find with a quick web search.

Over the years I have trained thousands of merchants on the basic functions of their payment devices. In many cases I found myself training people who had been using the payment device for years not knowing the difference between a void and a return. Looking back at our past blog posts I realized that we had never covered the four basic functions of a payment device. So that is exactly what we are going to cover today, and you might just learn something new that will save you time and a few dollars on your processing fees.

We are not going to get into the specifics of any one credit card terminal or Point of Sale system, since the operations of each system are different. However, these core functions of a payment device are so fundamental to payment processing that these operations should be easily accessible on your own device. The goal is to help you have an understanding of what these functions are and how, why, and when to use them.

The following are the training basics that I provided every merchant during my time in customer service and technical support. This information is a great place to start when training the people in your business.

The Basics:

There are 4 basic functions of every payment device: Sales, Voids, Settlements (batching), and Returns. In order to learn how and when to use each of these functions, first, we also need to understand the transaction life cycle.

Sales: When processing credit cards, there are two steps to the transaction: authorization and capture. When you select the Sale function on your payment device and process a transaction, the device communicates through the network to obtain an approval. If an approval is received, the device will store the approval code and flag that transaction for capture later in the day. At this point funds have not yet been moved, they have just been reserved for the business. This is typically the time when a cardholder might see a transaction as pending when looking at their online banking.

Voids: The merchant has the ability to make adjustments to any transactions that have been authorized but not yet captured. This is primarily used by restaurants with a tip line on the receipt, however, this also allows the merchants a chance to void a transaction if a mistake was made. The benefit to voiding is that funds are not transferred and therefore you are not charged the discount rate for that transaction. Keep in mind you will still have to pay the transaction fees, however, you will avoid paying the percentage charged on that transaction.

Settlements: At the end of the day, your terminal will need to be Settled (batched). This is the function that captures and finalizes the transaction in your payment device and starts the process of moving funds between the cardholders and your bank. Once settled, a transaction cannot be changed in any way. In most retail businesses the settlement process is automatic, however, you still need to review your settlement reports daily to verify that the settlement was closed successfully. This process is not always automatic and for some industry types, it is normal for a processor to not allow auto settlement. Whether automatic or manual, you should be verifying that the settlement report shows it has been successfully completed as this is what starts moving the funds to your account.

If there is any sort of error, or you are unsure if a batch closed, you need to reach out to your payment processor as this will cause delays in funding. It is also important to keep in mind that the settlement date is the date that will ultimately show up on the card holder’s statement and that any authorization over 24 hours old could be considered a higher risk by the issuer and may cause the cost of any such transaction to increase.

Returns: Think of a return as a reverse sale. Processing a return will pull money from your current batch or bank account and send those funds to a cardholder. Just like a Sale, the return must be settled before the funds begin to move. And subsequently, you can also void a return in the instance that there was a mistake entering the return. Keep in mind most processors will not charge you a percentage rate for the returned amount, however, you have already assessed a percentage on the original sale. A few interchange categories will automatically credit you back for the original sale after a return is processed.

Quick Recap:

A Sale authorizes the transaction and stores it for capture.

A Void deletes a transaction as if it never happened, used only prior to Settlement.

Settlement finalizes your transactions and starts moving money.

A Return is the reverse of a Sale, used any time you cannot void a transaction.

Important Tips:

There are many other functions on the standard payment device, however, for most businesses, these four basics are the only ones you will likely ever use outside of talking with your payment provider. Below are a few things to remember when using your payment device and why they are important to the security of your business.

friendly shop assistant ready to take orders on pos terminal

Customer-facing equipment is designed to give people outside of your business the options they need to complete a transaction. The business-facing device should not be accessed by anyone outside of your business.

There are a few bad actors out there who could cause all kinds of issues for you if they get ahold of your device even for a moment.

If anyone outside of your payment provider asks you to use a function that you do not normally use, that is a HUGE signal that you need to stop the transaction or contact your payment processor immediately.

There is one way to run a Sale, there are multiple ways to make it appear like you ran a sale when you didn’t.

Do not use your payment device to accept payments on anyone else’s behalf.

This makes you financially responsible for not only the fees generated but for any risk or fraud-related issues.

If at any time during a transaction you feel like something isn’t right, it is perfectly fine to tell your customer your credit card machine is not working and to call your processor’s support team for advice.

You know your customers, how they act, what they purchase… It’s common to hear a merchant say “Something about that sale didn’t feel right” when we are assisting them after they have been the victims of fraud. If it doesn’t feel right, pause and consult your processor.

Do not run your own card for more than $1.00.

I know there are some legitimate times when someone might be tempted to use their own credit card at their business. The problem is it could also be viewed as using a credit card to advance your business money, which breaks all kinds of rules that could be an article on its own.

A Brief Note on Liability:

When it comes to EMV(dipped) and NFC (Current Contactless) transactions, if the business accepts a stolen credit card, the issuer assumes the liability to repay the cardholder. If a transaction is swiped or keyed, the business assumes the liability to repay the cardholder. Avoid accepting swipe and keyed sales whenever possible. While this is not going to be an option for some businesses, you need to at least be aware of the risks. Cardholder protection comes at the cost of the businesses that either issue the cards or accept the payments, and that is strictly based on how the payment was accepted.

Terminal How-To Videos

If you are looking for more information on how to use specific lines of terminals, check out our video playlists linked below.

Many merchants have been looking to cash discounting to lower their payment processing costs because it’s a far easier way to offset processing costs than meeting the surcharging requirements. Today we are going to go over how cash discounting works and how it can help you offset your processing costs.

It may sound counter-intuitive that discounting a form of payment would help offset the setup costs of another and that’s because it is. The reality behind cash discounting is it allows the business to increase their prices across the board and then not pass that increase on to their cash-paying customers. Effectively when the merchant rings up a sale it gives them the opportunity to promote cash payments by offering a discount to the consumer. For those consumers who pay with another form of payment, they will be paying the increased prices of the goods effectively offsetting the additional cost of their form of payment.

Not only is cash a less expensive way of accepting payments, but cash payments also offer other benefits to the business. As mentioned before it gives the business an opportunity to offer a discount to their customers. Being able to offer a discount is always favorable to the consumer even if they are unable to take advantage of the discount at that time. It also promotes the use of cash by those same customers in the future helping increase the total amount of cash sales. Furthermore, gives more control of the transaction back to the business as consumers paying with cash don’t have the same protections as they would when paying with a credit card.

That doesn’t mean cash discounting is right for all businesses as there are some other sides of the coin that need to be thought about. For one thing, you are going to be increasing your prices slightly which may be a negative for some customers. Your business will be handling more cash which can mean additional bank drops, and/or a higher risk of theft. You will also need to train your staff to communicate the change effectively so cardholders don’t feel like they are being punished due to their form of payment.

Only you can decide if it’s a good fit for your business. If it is then setting up a cash discounting program is pretty simple. These days most point-of-sale systems have the ability to support it, and it’s just a matter of working with your payments and/or point-of-sale provider to set up the software correctly. Most payment providers have programs that help businesses set up and automate a cash discounting program. While this has always been an option for merchants in the past, the truth is for many it was a very manual process.

Please remember cash discounting is different than surcharging and that surcharging has very specific rules behind it. Please see our old article on Surcharging for more information. Also keep in mind that some things may have changed since the writing of the article, but the main idea of surcharging is well outlined.

If you have questions have Cash Discounting or Surcharging we are always here to assist you in any way we can. Feel free to reach out by phone or email.

When it comes to accepting credit cards there are a lot of rules and a lot of drab documentation to go with them. Many times businesses are breaking rules that they don’t even know exist. In this article, we are going to take a look at a few key rules, why they exist, and how they can affect your business.

For those of you who love really digging into rules and regulations, I have you covered as well. I have linked to the more than 1,300 pages of Visa and MasterCard rules to get you started. Spoiler alert, you will be asleep before you get through Visa’s 41-page table of contents.

Let’s jump in…

Accept All Cards

This is a band-related rule. If you accept Visa cards you must accept all types of Visa cards. The same goes for MasterCard and other card brands. Now there is some nuance depending on what country you are in, but for the most part, the rule is to accept one card from a brand you accept all cards from a brand.

It’s not good for anyone if businesses are checking cards and denying payments by customers with certain cards. Some of you might be wondering why on earth a business would do such a thing, and the truth different is cards can have higher interchange chargers than others increasing a business’s cost. Different card types may carry additional chargeback or fraud risks. While most of these are mitigated by contactless and EMV payment acceptance, not all businesses have the ability to accept payments in person.

From what I have seen merchants who try to avoid cards that they think cause higher interchange fees still end up accepting the same mix of cards, and all they have done is irritated some of their customers.

Surcharges

This is kind of a No No… The card brands would really rather you not surcharge the cardholders and it’s currently not allowed outside of the US, Australia, New Zealand, and Europe. Even where it is allowed there are conditions that have to be met before you are actually allowed to surcharge.

Here are the main requirements.

Surcharging must not be prohibited in your state.

You must notify the card brands and your processor 30 days prior to surcharging.

You can only surcharge credit-based transactions.

You can not charge more than your cost to accept the payment.

You must have proper signage and notification to your customers.

If you feel like surcharging is something you want to do I would start by reviewing your current payment processing setup and understand the fees you are being charged. From there reach out to your processor, or to us, and have a discussion about the requirements, and how you can comply properly. Then think about what effect that may have on the business both from an expense and customer perspective. At that point, you will know if it’s right for you.

There are also alternative ways to offset your transaction costs that are not considered surcharging. We will go over one such option in our next article.

Minimum Transaction Amount

In the past, this was not allowed, however for the US merchants are now allowed to have a minimum transaction amount as long as it doesn’t exceed $10. Again like with Surcharges this only applies to credit transactions. You cannot put a minimum on debit transactions.

Generally, it is not a good idea to put minimums on credit card transactions, it increases friction with your customers. That said for merchants who have many small ticket items this can help to greatly reduce their effective transaction cost. Imagine someone buying a pack of gum for $0.89, and the merchant paying as much as $0.43 just to accept the payment, when a $10 transaction might cost them $0.57. The $0.89 transaction has an effective cost of almost 50% whereas the $10 charge has a cost of 5.7%. Now yes both of these scenarios are exaggerated, but they really are not unrealistic for some small ticket businesses.

Don’t Run your own credit card

I can’t stress this one enough, just don’t do it…

Why? From the perspective of the card issuer and processor, they don’t know if you are buying something from your business or if you are loaning the business money from your credit card. If it was a loan to the business then it would be subject to other rules and at minimum have to be processed as a Cash Advance. Because of this uncertainty, it’s not allowed at all, with the exception of test sales at $1.00 or less.

There is also the potential for a merchant to attempt to dispute their own credit card transaction after either depleting the bank account or taking the product. This has come up a couple of times in businesses with multiple partners or owners, where one tries to steal from the business by using the credit card network. I can assure you that it doesn’t turn out well for anyone. From held funds to termination by processors and issuers, to potentially serious legal action.

For that matter, you shouldn’t be running anyone’s card outside of your day-to-day sales operations… If you need funding for your business there are other options that are legal and don’t jeopardize your business’s ability to accept payments.

Finally, Do not run credit cards for anything for anyone else

This tends to come up when a new business wants to use another business’s payment processing because their own sales are currently too low to support a merchant account of their own. At first glance, it doesn’t seem like there would be any harm done, but the devil is in the details. For one thing, the two businesses are likely selling different products and services which changes the risk profile of the business with the merchant account. Even if they sell the same products or services some of the transactions they process will show up with the wrong business name on them causing confusion for cardholders and increasing chargeback risk. Then there are processing fees, two businesses mixing funds, and potential disputes between the two businesses sharing this account.

But those are small potatoes compared to the real risk. If you are the business owner who personally guaranteed the merchant account you carry 100% of the liability. So if the person/business that is using your merchant account starts dealing in high-risk or illegal transactions it doesn’t matter if they were the one running the cards. You and your business are the only financially responsible parties. You may even run into some personal criminal charges as well.

Please avoid this at all costs.

Are you ready for the Rules?

As promised above, 1,300+ captivating pages. All joking aside it’s actually a really good idea to know what’s in these, at least the ones that pertain to your business. There is some really good information in these documents and a lot of time and effort has been put into them. Unfortunately, the topic just isn’t very exciting.

If you have any questions about any payment processing rules, you at least have a place a start looking. If you find your processor isn’t a great resource we are more than willing to answer or give direction on any questions that you have.

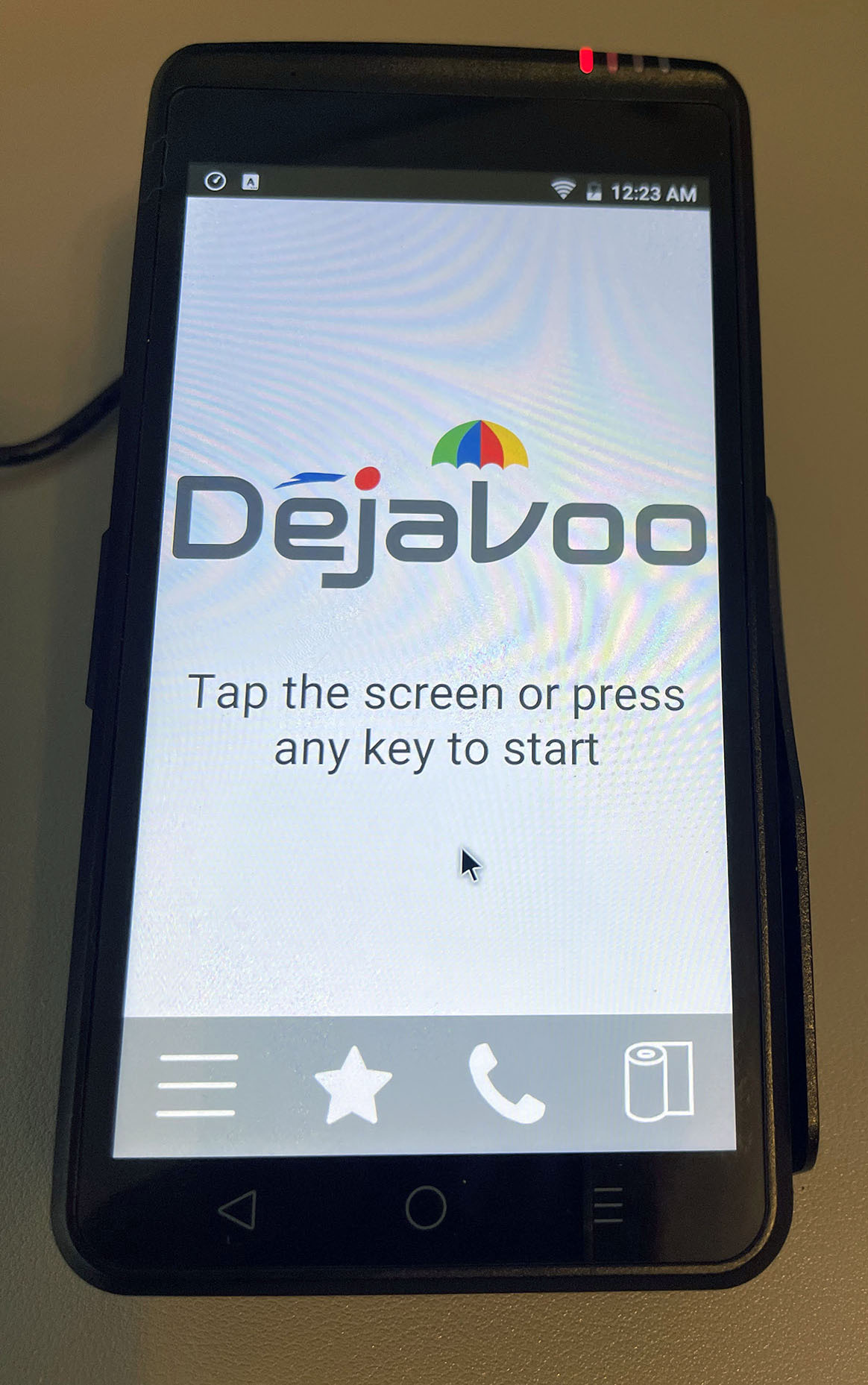

Dejavoo recently released the QD series of Android-based credit card terminals and we figured it was about time to put together a brief overview.

These new QD devices use Android as their operating system, that said Dejavoo did a great job of keeping the functionality of these devices the same as the Z line of terminals. Someone can easily switch between the two different series of devices and feel right at home.

QD Family of Devices:

Dejavoo QD3

Dejavoo QD2

Dejavoo QD1

Dejavoo has released 5 new devices so far in this line up as listed below. While each has its specialty these devices appear to be very flexible and could work in multiple business types.

The QD2s that we purchased for testing are stout terminals in a form factor that is similar to the Dejavoo Z line and most of the industry. Where this device really stands out is its 5.5″ screen size. The Dejavoo software doesn’t feel cramped on smaller machines, but on this one there is so much more space. The additional space and button sizes are nice to have on a full touch screen system, especially one that you are not holding close to your face.

Battery life definitely feels like it would last all day even under load, however, I didn’t have time to run a day’s worth of business through the device. My unit came set up with the power cable and Ethernet adapter screwed in place, which is not something I would expect for a mobile device. Nevertheless, it was easy to remove a few screws and clips to set this machine up for my use case.

It’s also nice to see Dejavoo has been thinking about cable routing and management. In some of their product slicks, linked below, you can see where they are routing cables in different ways depending on the device’s purpose. From what I am seeing on the QD2 you are not just stuck with cables that are forced to come out one side of the terminal. This will make it much easier for those of you trying to keep a clean counter.

You can see in this picture I have already removed the screws, I just had not removed the cables yet.

There isn’t much to say here, because the device has everything you need. EMV, Contactless, Swipe, Debit, and EBT if it’s a mainstream acceptance type you can process it.

I also like to point out that the contactless area is clearly identified for the consumer, as opposed to some devices that show they are contactless but you can’t ever seem to find where the reader is.

Communications:

Communication options on the entire line are wonderful. It has everything you want to see, however, there are a couple of things to note.

There is no phone port or Ethernet port integrated into the device, or at least in the QD2 I was working with. The Ethernet connection is via a USB dongle, which has its pros and cons. Yes, it’s another dongle you have to keep up with, however, it appears to be a standard USB Ethernet dongle. We purchased a random TPLink USB dongle from the local computer store and tried it on the QD2. Worked like a charm. That said not all USB dongles are going to be supported natively by Android OS.

Conclusion:

I feel like Dejavoo has another homerun device line with the QD series. These are robust payment devices that are loaded with the feature sets that businesses today need. The move to an Android-based system also opens up Dejavoo to additional options in the future, while delivering a SMART phone-style user experience. If you are in the market for a new payment device this lineup is something you definitely take a look at.

Interesting Techie Fact: Which I’m sure are not supported use cases.

Since the terminal has a single USB A connector for its USB dongle. For laughs, I connected my Logitech mouse and keyboard to it, and as expected both worked. For some reason, I couldn’t terminal to accept input from my keyboard’s 10-key.

I also tried plugging in a USB hub and was able to successfully process sales using a mouse/keyboard while also connecting via the USB Ethernet adapter.

Then I tried using the supplied Ethernet dongle on a test PC we have running windows 11. It was plug and play, Ethernet worked as soon as I plugged it in.

Would you place a stop payment on your previous merchant account provider if you found out you had some absurd early termination fee?

We recently set up a new client that was referred to us. He operates a very small business that manufactures and sells a unique product that fits a growing niche. He had previously been processing with a payments provider that either set up his account incorrectly or that was purposely charging him outrageous fees. As an example when we started talking to him about signing up with us he was effectively being charged 30% in payment fees.

He was clearly not happy with that situation and was ready to find a better solution. We promptly got him set up and operational. What we found out later is his previous provider was trying to charge him a $2,000 early termination fee. When he heard about this fee he opted to do a stop payment on the couple hundred dollars in monthly fees they were charging him. Unfortunately, he didn’t realize that many payment providers use the same backend services that handle funding. So placing a stop payment on his old provider effectively placed a stop payment on us. A downside with placing a stop payment on a corporate bank account is whoever was accessing your account is no longer allowed to re-attempt any transaction to that account. It’s designed to prevent re-attempted charges which makes a lot of sense. Unfortunately, that includes deposits as well. As soon as the stop payment was received we were no longer allowed to fund that bank account.

We worked with the merchant and his bank to get this resolved as quickly as possible, but the bank was unwilling to lift the stop payment as it would allow his previous provider to access his account as well. He eventually ended up having to go through the cancelation process with his old provider and pay the early termination fee. Again during this process, we were not made aware of this early termination fee nor that he was going to place a stop payment on them. If we had been aware we may have been able to coach him on maybe getting that early termination fee lowered or removed. At the very least we could have helped him confirm if placing a stop payment would have affected our ability to make deposits into his account. Between all the hoops he ended up jumping through closing out his old account, it took 25 days for his bank to give us written permission to access his bank account.

Stop payments have their place, but should really be used as a last resort if at all possible. You should also reach out to your payments provider and ask for advice especially when it comes to another payment processor. We see all kinds of scenarios concerning bank accounts that most businesses never run into. While most people see our primary function as access to card payments a lot of what we do behind the scenes is focused on making sure our customers can stay focused on their business. Any time we can help prevent a bank issue from occurring is an excellent use of our time.

When working with payment providers feel free to be upfront and let your provider know what you are facing. A great merchant account provider will that the experience to at minimum make sure you are pointed in the right direction and can help steer your away from any pitfalls.

This comes up more often than you might think, many attorneys out there misunderstand how payment processing may cause accidental commingling of funds if not set up correctly. While attorneys are familiar with IOLTAs, a trust account used to hold clients’ funds, they don’t always recognize the path they may be taking to fund an IOLTA could cause accidental commingling.

Generally, speaking attorneys who may be handling client funds will have at least one operating account used for accepting payment on complete work and running business operations. They will then have a second account for storing client funds like retainers or other funds that belong to their clients. While that seems easy enough getting funds into the trust account isn’t always so simple.

Sure if a client has the ability to write a check to your IOLTA account its just a matter of depositing the check. Its similar with Cash assuming you have the IOLTA account at a local bank branch where you can make the deposit. You see you can’t just deposit funds into your operating account and then transfer the same sum to the IOLTA. Yes, in effect it accomplishes the same thing, however, the rules are set up to prevent a law office from ever having direct access to their client’s funds.

It gets even more complicated when a client wants to pay on a credit or debit card. Many attorneys accept credit cards for payments for work completed but those depositing go to their operating account. Some attorneys like to set up a separate merchant account that allows them to accept credit and debit card payments that deposit directly to their IOLTA account. What people tend to not think about are the payment processing fees.

Imagine you get an IOLTA setup you add a merchant account as an additional way to fund that account and you figure you’re all set. The funds never hit the operating account, so many feel like they are in compliance. This still isn’t a perfect setup as the processing fees are charged to the IOLTA which is a cost of doing business that should be applied against the operating account, which is not allowed.

That said it is very easy to set this up right the first time. Its key to be clear with your payments provider about what you are doing and explain that you need the funds to deposit directly to the IOLTA account and any and all fees be applied to the operating account. This should not require any additional paperwork than a normal merchant account setup aside from maybe a second voided check or a bank letter. Generally, you will need to submit a voided check for each bank account that the payments provider will be accessing.

Most payment devices can even be made to support multiple merchant accounts meaning you don’t usually need additional hardware. We even have ways to accept payments via a web interface so you can operate from anywhere and don’t need any equipment at all.

If you have any questions about properly handling processing clients’ funds please reach out to us. We would be happy to tell you about options and make sure you get on the right path. It really is a simple setup and the right way to handle those funds.

If you accept tipped payments there are some potential, lesser-known, chargeback risks you should be aware of. For some types of tips, a card issuer is allowed to dispute any portion of a tip that exceeds 20% of the original sale. This is not the case with all types of tips, however, this does affect the most common tipping method for restaurants and bars. If you accept tips now or plan to accept tips you should be aware of the potential for chargebacks and understand why they might come through. Unfortunately, there is little that can be done to prevent the type of chargeback we are going to discuss, however not all is lost. While I really don’t like this set of rules, I also can’t see another way to handle it from an issuance perspective without serious changes to how cards are authorized.

Let’s set up some background: If your business does restaurant-style tipping with a tip line and a later tip adjustment you are at additional risk of chargebacks. For businesses like restaurants, bars, hair salons, etc. there is an allowance of 20% for them to adjust a pre-authorized transaction in order to collect their tips without processing an additional sale. If you are a business in an industry that does not have these allowances you are at additional risk of chargeback if you settle a transaction for any amount over its approval.

Not all businesses accept tips via tip adjustment. Many businesses that accept tips use a method that I will refer to as tip-in-transaction. This is a method of asking for the tip at the time of sale and including that amount within the original authorization. These merchants don’t have the additional risk that comes with adjusting the settlement amount after authorization. There are some businesses that could use this method, but prefer tip adjust so they don’t have to ask for a tip or have a device that prompts the customer during checkout. That said if you are doing tip adjust today you may have the ability to switch to tip-in-transaction if it’s a fit for your business.

Let’s get into the risks for those who do adjust their tips:

The risk comes into play once the tip amount exceeds 20%. Technically your approval allows you to capture up to 20% more than your original authorization. An issuer has the ability to dispute any amount above that 20% ceiling without even notifying the cardholder. The majority of the time this never happens and so most merchants don’t even realize that it’s something that could happen. Just because the card issuer has the ability doesn’t mean they will use it. In rare instances, I have heard about a chargeback originating from extremely irregular tips on very high authorizations. Most likely this is an issuer or cardholder thinking there was some sort of mistake when entering the tip amount or maybe even attempted fraud. To me, it makes sense that issuers and cardholders would need the ability to dispute tip amounts in these cases.

Recently I have heard of and reviewed a couple of instances where the amounts were small and quite normal. For example, one chargeback I looked at was for a bar. The authorization amount was $3.00 and the customer left a $1.00 tip for a total of $4.00. The issuer was disputing $0.40 of the total transaction. When I first heard about it I was thinking there is clearly some kind of miscommunication here, why would an issuer spend time disputing a $0.40 overage on such a common thing.

What was even more perplexing is that this wasn’t the only transaction we found that was being disputed on this merchant’s account. We found 3 more that were similarly small as the first. The highest dispute was for around $1.40.

Why would an issuer spend time disputing such small amounts?

As far as we could tell this is a pre-paid gift card. Not to be confused with a pre-paid credit card. Unlike Pre-Paid credit cards, the Visa/MasterCard/Amex gift cards, like the kind you get at the grocery store and are given out around the holidays, are not linked back to an individual person.

If a business puts through a transaction that exceeds the card’s available balance by authorizing one amount but settling a higher amount then that is a real problem for those issuers. When one of those cards is processed at a restaurant they likely check the balance of the card and only approve the sale if the card’s balance exceeds the authorization amount by 20%. This would be done to prevent losses while also allowing those cards to operate in a tipping environment.

This is where it becomes difficult to find a better solution.

When tips are involved the card issuer cant know what the cardholder is going to tip. On traditional credit and debit cards, this isn’t a huge issue. The issuer can increase the balance that is owed by the cardholder. They can also charge fees for going beyond the card’s limits, or even draw a bank account negative and collect the funds and fees at a later date.

For PrePaids they have to decide between setting a tip-ceiling or setting those cards to only work at businesses that don’t accept tips.

Maybe there is a better way that the industry could handle tipped transactions on prepaid cards. One possible way is at the time of approval to have a notice printed on the receipt that the card is unable to accept over its ceiling. That way the business and the cardholder would be alerted that the card can’t accept tips beyond 20%. This would not be too different than how partial authorization work now. For some card types, the issuer can approve a transaction up to the limit or balance of the card. When the payment device prints the receipt it clearly states the card was approved for an amount lower than the total and prompts the merchant to collect another form of payment for the remaining balance due. Doing this would allow normal cards to operate as they do today while preventing chargebacks on cards that don’t allow the cardholder to exceed the ceiling.

While that is easily stated it would likely require changes to both the issuance and acquiring side of the industry. It would also take time for businesses and consumers to adapt to these changes. Businesses would catch on quite quickly, but it would likely require businesses to explain to their customers that their card has a hard tip limit which I would assume would be an annoyance at best to the business and the people receiving the tips.

People who work in tipped environments are not going to be happy about telling people they are not allowed to tip you above 20% due to the limits of their payment method.

While the amounts are small, the costs add up.

Some of you may be thinking it’s $0.40 here or there, and this doesn’t come up very often, what’s the big deal? It’s the chargeback fees. If you’re paying $15+ for each chargeback then that $0.40 overage likely costs you more than the revenue from that sale. Four chargebacks quickly because $45+ just in fees. In this particular instance, we manually waved the merchant chargeback fees but that isn’t a long-term solution.

While this isn’t a common issue, it’s one I would like to see addressed and changed. Hopefully, this is something that is in the works. In the mean, it is rare and is just something to be aware of.

You can find the actual rules from Visa here. The purpose of this article is to alert people to potential risks and is not designed to be a comprehensive guide. In order to keep this article from going on for pages, we encourage everyone to review Visa and MasterCards guidelines and understand how they may be applied to your business.

Here we look at 5 more ways to accept payments that are generally much cheaper than most businesses expect. Just like in our first 5 ways, many of these do have an additional transaction fee that is part of the overall billing. That said those fees are generally in pennies per transaction and if they increase sales or operational efficiency, they will be a negligible cost.

Virtual Terminal

Many businesses out there operate with a standard credit card terminal even though they don’t do any card-present transactions. A virtual terminal sets you free from needing to be at your device to process payments. You also get the benefits of full data reporting, easy access to payment records, and simple ways to process refunds without needing the card data. Unlike traditional terminals, there are no up-front fees to just have a virtual terminal. You will generally pay around $5.00 monthly.

2. IOLTA Accounts

If you’re not an attorney you probably want to skip this one, but if you are you don’t need to pay for specialty software just to properly handle your IOLTA account. We have simple setup options that prevent any co-mingling of funds while properly routing fees through an operating account. Some of the systems out there can cost an arm and a leg and include many features that you do not even use. We can handle your setup for as little as $12.00 per month in addition to your normal merchant account fees.

3. Online Check Processing

Check processing has its own set of fees separate from processing credit/debit cards. Many online check offerings have even more fees piled on top for risk assessment purposes. The truth is for traditional check conversion most of the time there is not a need for those additional risk assessment fees. For most businesses, we can eliminate the need to have an expense check reader and the need to take a check to the bank for a deposit for as little as $12 per month.

4. Gift Cards

We find that many merchants do not look into gift cards because they feel their business is too small, but we have seen some of the smallest businesses leverage the power of gift cards. While there is a small upfront cost of getting cards printed and shipped, you can start with a small order to get started. From there you can work gift cards into your sales approach. The monthly and transaction costs of gift cards vary, and the options won’t fit in the scope of this list, however, they are quite reasonable, and many times work with your existing payment hardware.

5. Cellular Payments

Cellular processing options are quite different than they were in the past. From options to process payments on your phone to Wi-Fi terminals that you can tether to your existing wireless plans, it has never been more cost-effective to process over a cellular connection. The traditional cellular terminals still exist and are a great option for some, but for many just are not worth the additional costs. If you are looking to expand into cellular payment processing, there are many options that can be started for just a few dollars a month.