If your business is in need, there are several loans and programs to help you get through these uncertain times. There is a lot of good information on the Small Business Administration’s COVID-19 webpage.

Coronavirus Relief Options

The Paycheck Protection Program (PPP) The PPP is an incentive for small businesses to keep existing employees on their payroll. These loans will be forgiven if the business keeps all employees on payroll for eight weeks. The money can also be used for other qualifying business costs.

This program is available to almost any business with 500 employees or less, including non-profits, veterans organizations or tribal business concerns. It also includes sole proprietors, independent contractors, and self-employed persons.

If you feel that you would not qualify due to past credit issues, or liens, it is still worth contacting your bank and asking about the loan. This program is designed to keep companies business-ready, and from what we are hearing, past issues have not been a problem for businesses applying for this program.

Remember, your depository bank will be making these loans so you should contact them directly. If for some reason they are not participating, you can always reach out to another bank, however, they may require that you open other accounts with them.

Economic Injury Disaster Loan Emergency Advance (EIDL) The EIDL is designed to provide economic relief to businesses that are currently experiencing a temporary loss of revenue. According to the SBA, this loan advance will not have to be repaid. The business eligibility appears to be the same as with the PPP above.

You can go to https://covid19relief.sba.gov/#/ to begin the application process. It starts off with a quick eligibility verification section, and if your business is eligible, you can continue to the application.

SBA Express Bridge Loans Express Bridge Loans are for small businesses that already have a business relationship with an SBA Express Lender. For those businesses, you can access up to $25,000.

These loans can be term loans or used to bridge the gap while applying for a direct SBA EIDL. This loan is expected to be paid in full or in part by proceeds from the EIDL.

SBA Debt Relief The SBA Debt Relief program will provide a reprieve to small businesses by paying principal and interest of current 7(a) loans, 504 loans, or microloans for a period of six months. They will also pay the principal and interest of new 7(a) loans issued prior to Sept 27, 2020 for a period of six months.

In response to COVID-19, most card brands are opting to delay their scheduled rate adjustments. Below is a table showing which card brands have delayed their rate adjustments, and when the changes have been rescheduled.

Card Brands delaying until July 2020

Visa

MasterCard*

Discover

American Express^

Star

ACCEL

^American Express Opt Blue’s assessments and inbound fee will be pushed back to October 2020.

*MasterCard Puerto Rico Domestic and International Dues and Assessments fee will still be implemented in April 2020.

You should always have a fraud prevention plan, but in the wake of coronavirus, there is increasing pressure from criminals trying to take advantage of the confusion and stress on businesses. Now is a good time to review some of our past articles on protecting your business, see the link list below.

Avoid doing business with people who try to get you to accept payment on a credit card and ask you to give money to another party. This is not how credit card transactions are designed to work, and the card you are accepting is most likely stolen.

Also, any email communication or software related to COVID-19 needs to be verified before you interact with them. There are phishing emails and fake apps that are designed to defraud your business. Be extremely cautious about any solicitations from unverified sources.

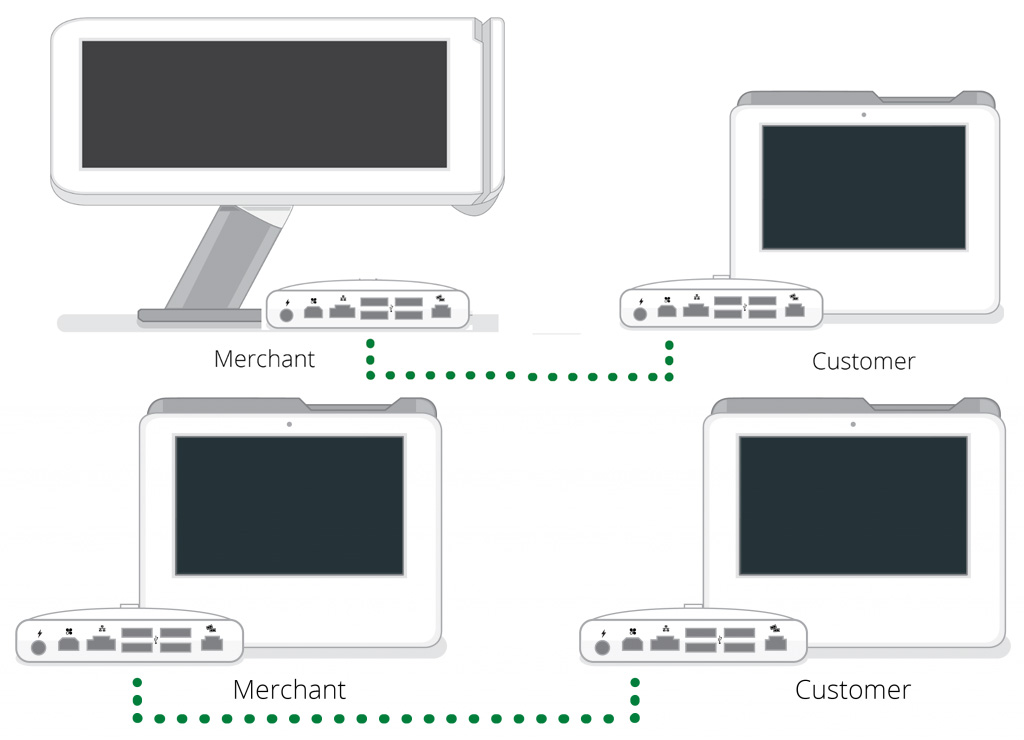

In this newsletter, we are going to look at different ways your business can continue to process customer payments as well as introduce a way for merchants to protect themselves during this difficult time. Many businesses have been turned upside down, and now more than ever each merchant needs to be informed on various ways to utilize their merchant account.

Gateway- Virtual Terminal

Offices, restaurants, and many other types of business have been forced to close their physical locations. For most, it is imperative to find a way to continue to accept customer payments in another way. Setting up a virtual terminal is a great solution to fill this void. A virtual terminal enables the business to accept payments anywhere an employee has access to the internet. The card information is keyed into the virtual terminal, and the payment is processed just as any transaction would be. We have had many requests for this service from merchants, and for most, the set-up process is quick and simple. Depending on your current processor, additional charges may be required. Typically, it is an additional monthly charge to pay for the service, as well as an additional transaction fee.

Customer Facing

Recently, we have fielded many requests for alternative payment solutions. Many merchants have simply stopped accepting cash payments due to contamination, and many more merchants have requested some sort of customer-facing device, so their employees do not have to handle customer cards. We suggest speaking with your processor to see what type of options they have for customer-facing payment processing. One of our most popular devices is the Clover Mini with a rotating swivel stand. As well as having access to one of the more robust systems in the industry, this option keeps the merchant from ever touching a customer card or exchanging receipts. There are many options in the industry, but now more than ever is the time to take precautions for the protection of your employees.

Cash Advance

It is no secret during this difficult time, many businesses are having trouble maintaining a steady income stream. Business owners may have access to existing solutions that they may not be aware of. One such solution is a cash advance by your merchant service provider. Cash advance programs are quite simple when compared to modern business loans. Businesses are approved for a cash advance based on their past processing history. As an example, a business that averages $10,000 monthly through their merchant account can typically qualify for up to a $10,000 cash advance. These cash advances are typically paid back through the merchant’s own credit card processing. A percentage of each batch is taken through the merchant account (typically 10%) until the advance is paid in full. These advances can be used to pay for anything the business may need with no restriction and no interest. It is to be noted that these programs may differ greatly depending on your processor, but programs like this exist for the very reason they may be needed today. A good credit card processor will do anything within their power to keep you processing and support you as a business partner.

Please note these programs and services vary depending on

your processor. This information is based on experience, and what The Merchant

Store is doing for our merchants. We are here to talk! Any questions, concerns,

or interest in our services please contact us!

This seems like a perfect time to talk about contactless and customer facing payment options. In a world of social distancing and constant hand washing there is even more reasons to limit touching other people’s belongings. The point of sale is one of the primary physical points of contact between a business and its customers, and customers and eachother. We are going to explore some processing options that you can implement in order to limit physical contact at the point of sale.

Contactless Payments: Most modern credit card terminals and PIN Pads are capable of accepting contactless payments via Near Field Communication (NFC). NFC is what is used by Apple Pay, Samsung Pay, and contactless credit cards. The nice thing about this option is the consumer’s device or card never leaves their hand and never comes in physical contact with the physical payment components. All the customer must do is hold their device or card within a couple inches of the point of sale and the card or device will begin the transaction process. Contrary to what you may think, this method is extremely easy. Once setup all the clerk needs to do is use the credit card terminal like normal and the consumer does the rest.

If this is not already functioning on your device, in many cases it’s just a matter of a software update. If you don’t already have an NFC capable device, they are quite inexpensive. For most new processing customers, we can provide NFC capable devices free of charge.

If you do have a contactless device, all you really need to do is start promoting it. We offer free Apple Pay stickers for merchants to help get the word out. You can also ask your employees to inform consumers that they may pay through NFC. Sure, not every consumer will know how to do it, but for those who do, simply reminding them that it’s an option will do a lot to limit contact.

Customer Facing Devices: You have seen these kinds of setups everywhere. The store clerk rings up a transaction and the consumer completes the transaction via a second consumer facing device. This can usually be setup very inexpensively if need be. If you have a standard credit card terminal, many times you can add an EMV + NFC enabled PIN pad that can act as your customer facing device. If you have a full feature point of sale system, PIN pads might work, or the POS vendor may have many different options.

If you have a Clover or are looking at switching to a Clover POS you can use PIN pads, or you can even use a secondary device like an additional Clover Mini as your customer facing device. Keep in mind if you have a Clover Mini, you are already setup for contactless payments that we discussed above.

Online Payments: Online payments aren’t just for retail eCommerce. Many restaurants today offer online ordering with at-location pickup or delivery. There are several larger retailers that have made this option available over the past few years. But, this option isn’t something only large companies have access to. Keep in mind, this path will take some additional planning on your part, and you may be required to setup an additional merchant account to separate the internal retail transactions from the ecommerce transactions. You are also likely going to see a higher cost per transaction for those keyed, but that cost increase could be negligible if you are able increase or even maintain sales.

Invoicing: We are able to add online invoicing to any new or existing merchant account for just dollars per month. This option allows businesses to submit email invoices to customers with a link to pay that invoice over the internet.

Online invoicing enables consumers to pay without having to meet up physically. This capability is great for service businesses, and we have seen unique ways other merchants have also used this option. While this may not be for everyone, it’s another great tool that can be very useful for many businesses.

Conclusion: We are all in this together and finding ways to better serve each other doesn’t just help improve things today, but also opens your business up to more growth once we get these difficult times behind us. If you have any questions don’t hesitate to call or email us. We are here to help in any way we can and will always provide the best information to help you make an informed decision.

Dejavoo was founded by the original founder of Lipman USA, and seems to be founded on the same principles that Lipman was: rock-solid products that are easy to use and very reliable.

Dejavoo Z8- Countertop Terminal

The Z8 is one of the most widely used counter-top terminals in the industry. Able to connect through Ethernet, dial, or using WiFi it captures payments for the modern customer using a touch screen display and built in thermal printer. A 2.4-inch LCD backlit screen gives the business owner and customer an easy to use payment system. With swipe, EMV, and contactless capability, the Z8 can accept payments from even the most Apple or tech. savvy customer.

Dejavoo Z11

While the Z8 is a very commonly bought and used terminal,

what is not set in stone is the price tag. I have heard quotes from processors

upward of $800 for this terminal. It is of note that the Z8 is a simple, easy

to use, standard terminal. By doing just a little bit of research, a business

owner will be quick to note their processor is marking up the price tag by

upwards of 300 percent at times. If your processor is marking up something as

simple as equipment for you to use (which you as a business owner need to even

process) how much do you think they are marking up your rates? Don’t settle on

overpriced processing and equipment, become a Merchant Store partner.

The Z9 essentially asks the business owner exactly what how

they want to process. With the wireless capability able to connect through

Wifi, or using a 4G/3G network this terminal does it all. This terminal features

EMV, Swipe, and contactless payment methods which you can take anywhere that

your cell phone works. With an upgraded battery that enables any business owner

uninterrupted processing, the Z9 is the go-to for many mobile, retail, or

restaurant businesses. Another unique feature of the Z9 is the ability to queue

customer support to call your business directly from the terminal by pressing

the F4 button.

Much of the same on quotes when it come to pricing and mark ups with various processors on the Z9. But I recently ran into even more of a horror story with a business owner. “John,” the business owner was just starting his business, his local rep. suggested the Z9. Without a lot of capital starting the business, his sales rep. suggested bundling the terminal cost into his fees. Essentially signing John up for a lease to own at the price of 39 dollars monthly. After a period, John saw the Z9 for sale for 4-5 hundred dollars. Realizing the terms of what was sold to him, John realized 39 dollars for 48 months wasn’t an ideal situation. While this is hopefully an isolated incident involving a deceitful sales representative, it is all too common of a practice. As is common in almost every business, if you are paying too much for one aspect, more than likely you are paying too much for every aspect.

Dejavoo Payment Software

Our team recently did a full demo on Dejavoo’s new payment software & cloud POS Technology. It seems this is Dejavoo’s answer to other software systems such as Clover, Lavu, Shopkeep, Revel etc. They have made every facet (including price) highly competitive to other similar programs. This software is tailored to virtually any business with specific setups for retail, restaurant, and a specific setup for salons and service businesses. This software is so specific we had to stop the demo for over saturation of information. That does not mean that it is not easy to use, what it means is that this software can be tailored to exactly what the business wants as far as inventory, employee management, item configuration, merchandise tracking, customer management, restaurant specific management, basically its got how ever robust a system as you need.

One of the biggest benefits with this software, is the all inclusive manager portal. Designed to give the business owner oversight over their entire operation. The simplicity of the system is also the equipment. Compatible with most standard tablets that require a simple download, the program is able to communicate and work seamlessly with an existing Dejavoo terminal. This means instead of expensive thousand dollar set-ups, a business can utilize specific software for as much as a computer and a Dejavoo terminal. Whether on the move, pay at the table, or at the counter top everything functions together and can be seen through the friendly master portal.

To Finalize

Dejavoo is moving in the right direction when it comes to equipment and software. At the Merchant Store we utilize and count on these terminals and software for our merchants, and trust the Dejavoo is constantly striving to improve, and stay up to date with the latest in security and technology. It is worth a look for any business to see if this could be the most beneficial, and also cost effective solution for their business.

For information, to schedule a demo, or to receive quotes on equipment please feel free to contact The Merchant Store (888-898-3436) or visit www.merchantequip.com

In short, no. You may have received marketing information describing the perfect world of having free credit card processing. While it is possible to establish an account and have the business pay zero processing fees, it simply means that those fees are being assessed to someone else. Welcome to the new world of merchant services, it’s called Cash Discount.

Let’s go through a scenario. It’s a new year, and you want to maximize your profits and are looking at ways to cut down on your costs. One of the most obvious ways is to reduce what you pay on processing fees. Looking over your processing statements, you equate your effective rate to 4 percent. So, for every $100 dollars you are receiving, you are paying $4 effectively. You call your processor, and the sales agent mentions a program called Cash Discount, which essentially takes away the cost of your processing fees.

How does this work?

Enrolling in a Cash Discount program, your processing fees will be passed onto your customers. While it differs between processors, the standard is around 4%. One way this works is by increasing retail pricing of goods and/or services by 4% and then offering to discount the sale by the same percentage for certain forms of payment. Usually the discounted form of payment is cash, but you could also give discounts to any other form of payment like checks or in-store gift cards. If you are interested in details about the other ways this is being implemented check out are article entitled, Tired of paying credit card processing fees?

It is important to note; customer satisfaction should always be a considered, which is why this model may not work for everyone. It is up to the business owner to see if and how this model will fit into their business. While a 4% increase to retail costs may be unnoticed by some consumers, others might be a more price sensitive. Businesses need to know how they can best explain the their discount program to their customers in the right way.

Cash discounting has been around for 20+ years, but its really starting to pick up steam. It would be surprising for anyone who regularly uses credit and debit cards to have not been offer a discount to use cash, or discount reversal percentage at the bottom of their credit card receipts. There has been some backlash in the industry, calling the cash discount nomenclature just a name for an additional surcharge. Some even calling for its outright ban, and unconvinced of the longevity of the practice. In any form, as of the beginning of 2020, many business are rushing to get in and offset their processing costs. Business owners are beginning to see a vast expanse in the array of various cash discount applications, programs with processors, and pressure from sales agents to investigate the programs and see if it is right for their business. While the program seems like a simple concept, there is a difference between surcharging customers, and offering a true cash discount.

VISA has mandated the program to abide by certain regulations. While the practice is completely legal when done correctly, where the grey area lies is the difference between a cash discount and a surcharge program. A true Cash Discount program is when the businesses list the credit card prices for the goods and discount the 4% or whatever the processing fees upon payment in cash. A surcharge program (an extremely common practice, and considered by some to be mislabeling of cash discount), is when the prices posted are for the already discounted cash prices, and the processing fees are charged on top of the listed price to the customer. According to VISA, the practice of the surcharging is against its regulations. The Durbin Amendment, made surcharging against the law for debit cards altogether. Additionally, specific states have set laws against Surcharging practices all together (CO, CT, FL, KS, MA, MS, OK). It is important for each merchant to do their research to determine exactly what type of program they are getting into, and whether it is in line with the standards and practices set-forth by card associations.

To summarize, it is worth any retail merchant to investigate whether this practice is right for their business. In the long run, this practice has the potential to save the business hundreds, or even thousands of dollars per month. While the program may seem like a savior to some businesses, it’s not going to be for everyone. It is also important that if a business implements a method of cash discounting that they continue to look for changes in regulations and laws, and make sure everything is above board because changes are always taking place.

If you have any questions we are always willing to lend whatever knowledge we have. Feel free to reach out to us at (888) 528-0058 .

What is is my contract length? Can I cancel my service without penalty?

Every merchant is under a contract with their processing bank, whether there is a penalty to cancel service is another aspect. It is also possible that your processor has helped supply your business with equipment, which in this case you will have to work out a repayment or return of that equipment. Contracts vary depending on which processor you choose, it is important to go over the terms and conditions prior to signing and being aware of any penalty for canceling the service. Some aggressive contracts may include liquidated damages provisions which basically make the cost of terminating, what the processor believes they would have profited on the account for the entirety of the contract. For higher volume merchants this can be tens or even hundreds of thousands of dollars.

What are my monthly

fees and processing rates?

Processing Rates

Depending on your business, these fees will vary. For instance, if the business is eCommerce, or keyed entry, the fees will differ from a retail business. Each merchant is charged a standard interchange fee from the card issuer, this fee cannot be waived. Your actual cost will depend on what the processor marks up above interchange. It is important to note that interchange will vary depending on the type of card and how you are accepting it.

There are over 800 interchange categories and each can have a different cost. Its easy to get caught up in all of the minutia and miss something seemingly small that ends up costing you later. A potential processor can perform rate reviews and show you an apples to apples comparison between your current rates and what they can offer.

In order to have a processor to provide you a real comparison they will most likely need a copy of your processing statement. That said before you send your statement to a processor its important that you ask them what fees they are quoting you. You have a real advantage over the processor when you ask them to quote you rates, and then ask them to do a comparison to show you how those numbers work out. This way they don’t see what your paying now and just slightly undercut it.

Monthly Fees

Standard monthly fees apply for all business. Typically, merchants will be charged a statement fee, but depending on the services being provided and the specific processor, there may be other fixed fees. Each processor writes accounts differently based on the type of business and processing history. Some of the fees can be waived, but it is important to note that some of these fees are being charged directly from Visa and MasterCard are are typically passed through to the merchant.

Make sure to ask each processor what each monthly fee is for. If you are reviewing multiple processors you will find that many of the fees are the same. Any fees that are outside of the norm should be questioned.

General rules of thumb: Retail – Monthly fees should run $20 or less even if you don’t process in a given month.

eCommerce and phone order – You should expect your monthly fees to be the same as retail, however keep in mind you may have an additional monthly fee for a payment gateway or virtual terminal. Generally these run between $5.00 and $15.00 per month in addition to the merchant fees.

What kind of Equipment do you suggest for my business, and what are the costs?

Using the right equipment tailored for your business, is not only important for your customers convenience, but also for the business’s fees and costs. It can be a burden for any business getting caught in an expensive lease for an extended term, especially if that equipment is unnecessary.

See future Newsletter: “Leasing, the Little Upside with

Major Pitfalls.”

Equipment costs vary depending on the processor, some will provide free equipment for the use of the business, while some mark prices up to turn a profit. If your processor suggests a piece of equipment at a specific price, it can be beneficial to do research and learn precisely what that piece of equipment costs on the open market. You would be surprised how much some processors will attempt to charge for equipment.

Can you perform a

rate review for my account?

If you feel you are paying too much for your credit card processing service, simply ask your sales agent or processor to perform a rate review for your business. Sometimes there are minor changes that your processor can do, and they can make a major impact.

For example, if you are using a terminal that is out of compliance, you may see additional charges on your monthly bill. Simply by upgrading your equipment, could reduce your overall effective rate drastically.

Another example is perhaps your account was initially written with the wrong fee schedule for your specific business, and by switching to a new rate structure you can reduce and prevent additional fees.

It is not out of the realm of possibility that your processor or agent would refuse this service, or simply tell you that your fees cannot be lowered. If this is the case your processor should be able to explain in detail your fees and why they’re not able to be lowered. That said don’t take their word for it. Call around and ask other companies what their rates are, and then ask them for a side by side comparison of current statement.

Some times you find that the deal you have with your processor is really good. Some times you find that you can save a lot by switching. Either way its worth contacting a couple companies.

How much am I paying for my PCI compliance?

As mandated by higher authorities that make up this industry, every merchant must be certified PCI compliant in accordance with the Payment Card Industry Security Standards. Quite a mouthful. Each processor is responsible for making sure their merchants are secure and the fees for this service will vary depending on the processor. Some charge monthly, some charge annually, and some processors may charge you both an annual fee with a nice monthly fee as well. It is important to be compliant and certified and it is probably more important to you to not be overcharged for taking a simple survey or having a scan performed. Your processor should be able to easily explain how much and when they will charge you.

While this fee is generally not negotiable with any given processor, they each have their own deal with PCI security assessors and so the pricing to the merchant will vary from one to another. Generally speaking this fee should come out to between $90 and $120 per year while compliant. Non Compliant accounts are generally assessed around an additional $20 per month until they become compliant.

Who handles customer service after business hours or on holidays?

Hopefully you process with a company that has excellent customer support. That said, sometimes that support is not available at all hours of everyday. It can be imperative to the business owner, to know how their processor provides support after normal business hours, and on holidays in case any issues arise. The last thing a business needs on a weekend or holiday when their terminal goes down is to get an answering service when they need to be processing cards.

Also a help desk is testable. Feel free to call into your processors help desk and see how long it takes them to answer, how they act on the phone, and how knowledgeable they are. You can also ask them about specific fees on your quote. While the help desk probably wont have access to your quote you can ask them what their company typically charges for X, Y, or Z. You can compare that information to the quote that was provided. This wont always work as some support people don’t handle the rate side of the business, however its worth asking a question or two.

Lets boil this down.

We have gone over a lot of information here so lets simplify it. If you are looking at changing processors ask them what their rates are, then ask them to breakdown your statement. Keep your monthly fees at or below $20 per month if your retail and $30 per for other businesses. Ask for no early termination fee and never lease processing equipment. Most importantly reach out and ask for help. People in this industry will bend over backward to lend their knowledge to those who ask.

If you have any questions we are always willing to lend whatever knowledge we have. Feel free to reach out to us at 800-937-3850.

There are two sides to a credit card transaction; Authorization and Settlement. Between these two stages of the transaction process there are 4 basic functions to all credit card terminals. In this write up we are going to go over both sides of the transaction and each of the basic functions in detail. While this is going to be a highly simplified explanation it should be more than enough to firmly grasp the concepts and proper use of a standard credit card terminal.

Sale:

Running a sale on a terminal initiates the authorization side of the transaction. This is when the terminal communicates and makes the approval request. If that request is approved the terminal will receive an approval code from the issuer and the transaction is stored in the terminal until the settlement is processed. At this point the transaction has only been authorized and no money has been moved and you are still able to alter the transactions.

Don’t confuse the Sale function with functions like Authorization Only. While auth only is outside the scope of this writing, it is not the same as a sale.

Settlement:

The settlement process finalizes all transactions processed on the terminal. This is the point when funds begin to move, discount rates are charged, and you are no longer able to alter transactions.

Transaction manipulation for most businesses refers to the voiding which we will get into shortly. Still other businesses like restaurants or lodging may utilize tipping or check-in check-out functions. You can only manipulate a transaction before it has settled.

If your terminal is set to automatically settle each day it is a good idea to review your settlement report to make sure it shows the batch settled successfully. It’s ultimately the merchant’s responsibility to verify that the terminal is settling.

Void:

A void is a type of refund that is done before a transaction is settled. When you void a transaction, it keeps the funds from moving, and therefore keeps the business from having to pay discount fees on the original sale. Voiding effectively just deletes the transaction from the settlement entirely. This results in the card holder seeing a pending transaction on their account for a few days before it eventually disappears.

There is also a function called a reversal which voids the sale and contacts the issuer requesting that the authorization or pending amount be released back to the card holder. For some devices this can be included as part of its batch function, for some it’s a separate function, and for others it’s not an option at all. If you have a reversal option on your terminal you should contact your processor for information about how to use it, as it’s a better customer experience.

Return:

If a transaction has already settled and you need to refund the card holder, your only option is going to be to perform a return. Unfortunately, that means funds will have already started moving and you are going to be charged your discount rate for having settled the sale. You really shouldn’t be charged an additional percentage for the refund however, we have seen processors who did charge their merchants for returns as well. If your processor charges an additional discount for returns, then it’s probably a good time to look for other processing options.

It’s also important to note that it is extremely important that you refund card holders the same way they originally paid. For example, don’t give a cash refund to someone who paid you on a credit card. The reason is there is no paper trail for the refund. If the card holder contacts their issuer and disputes the original transaction, you cannot prove you refunded previously, and will most likely lose the dispute as well as the money you already paid. Also, if a customer pays cash you wouldn’t want to refund them on their credit card, as that could cause some risk related issues on your merchant account.

Conclusion:

There are many functions a standard credit card terminal can do. For most every merchant these are the only 4 you will ever use. If a customer or issuer ever tells you to use a function that is not listed here, you should immediately contact your processor and explain the situation and get support on whether you should do what they are asking. Card holders and issuers should not be trusted when it comes to how to process sales or refunds. Many times, they will be trying do something fraudulent, other times they could cause problems down the road for you just due to their lack of understand the functions they are asking you to use.

MasterCard has entered phase two of its Dispute Resolution Initiative (MDRI) and so we felt that now was a good time to shoot out some information about what has changed in the world of chargebacks and what changes are still on the horizon. But first some history…

While credit itself has been around about as long as the world’s oldest profession, it wasn’t until the 1950’s when Diners Club released the first credit card, for our modern system of credit issuing and acceptance to take form. In the mid 1970’s, chargebacks were introduced to help build consumer confidence in a time when many people were still wary about revolving credit accounts. Since then times have changed and the credit card along with them.

The credit card industry is in a constant state of change, but it requires deliberate effort to make those changes. The chargeback system is a part of the industry that has been largely neglected for the past 50 years, but a year ago that started to change.

In April 2018 Visa released its Visa Claims Resolution (VCR) initiative which was a major overhaul of its chargeback system. VCR was designed to stop fake or fraudulent chargebacks as well as streamline the entire chargeback process. Before VCR, the average chargeback resolution time-frame for Visa was a whopping 46 days, with some disputes continuing for more than 3 months. Visa’s new chargeback initiative has just turned one, and it’s still too soon to tell how it will mature, so far there have been mixed reviews at best.

Unlike Visa, MasterCard is rolling out its new system relatively slowly in 4 phases over 18+ months. Phase one started in Oct 2018 requiring issuers to collect more information from cardholders before allowing a chargeback for a number of reason codes. This additional information should help MasterCard weed out invalid disputes before they start attempting to limit outright fraud on the part of cardholders who issue deliberately false chargebacks, typically known as friendly fraud.

Phase 1 – Affected Reason Codes:

4831 – Incorrect Transaction Amount

4834 – Point of Interaction Error

4853 – Cardholder Dispute

4863 – Cardholder Does Not Recognize

Phase 2 is where we catch up to present day and effects how merchants handle chargebacks and refunds. Basically, if a business receives a chargeback under these new rules the business should not refund the original transaction. Instead the merchant should continue to work through the chargeback process and let that process handle the funds.

If a business receives a chargeback and later decides to refund the card holder, even after winning that chargeback, the issuer can still issue a second chargeback resulting in the business being out the money twice. While there is a way to contest the double debit it would be easier to just not have to deal with that in the first place.

This phase also shortens the filing time frame on reason code 4834 (Point of Interaction Error) from 120 day to 90. It also removes two reason codes all together.

Phase 2- Affected Reason Codes:

4834 – Point of Interaction Error – Chargeback time-frame lower form 120 to 90 days.

4840 – Fraudulent Processing of Transactions – Removed as a chargeback reason code.

4863 – Cardholder Does Not Recognize – Removed as a chargeback reason code.

Phase 3 is an unknown at this time. We know its scheduled to start in October 2019, however MasterCard has yet to state what exactly this phase is. We will post an update as we get more information about this phase and what to expect.

Jumping to April 2020 and beyond, phase 4 will stop allowing subsequent chargeback reason codes. Instead, issuers will be able to continue a dispute with pre-arbitration which is very similar to Visa’s new setup.

Only time will tell how effective these changes are at improving the chargeback system and minimizing bogus chargebacks. So far, just based on Visa’s VCR initiative, we wouldn’t expect too much, at least initially. It is promising to see both Visa and MasterCard taking steps in the right direction. However, it may take many years before we see any real improvement at the merchant level. Until then, we will move forward cautiously optimistic that associations are attempting to level the playing field and making the chargeback process more fair to merchants.